Established retail banks worldwide continue to lag behind in creating an effective omnichannel experience, as a result customers are switching to competitors who offer them a more personalized experience. It is perhaps the most important conclusion from the World Retail Banking Report 2022 by Capgemini Invent and Efma.

The research is based on insights from two primary sources - the Global Voice of the Customer survey (with 8051 respondents) and Executives surveys and interviews (with 142 bank executives). Altogether, the research sources used include insights from 29 international markets.

Furthermore, the report shows that consumer expectations of digital banking have increased significantly. However, banks are struggling to meet these expectations because they lack data analytics capabilities. Now that customers can change banks with the touch of a screen, the researchers say it is critical that banks make better use of data and artificial intelligence (AI) to improve the customer experience, create stronger relationships and maximize customer value.

Analysts at Capgemini and Efma write that the rise of fintechs has brought about a paradigm shift within the financial sector, as expectations about the banking experience of consumers have changed. This would challenge the revenue and relevance of many traditional providers.

For example, the quantitative Voice of the Customer survey would reveal that as many as three-quarters of respondents are attracted to the more flexible fintech newcomers because they offer fast, easy-to-use products and experiences that are readily available while costing little.

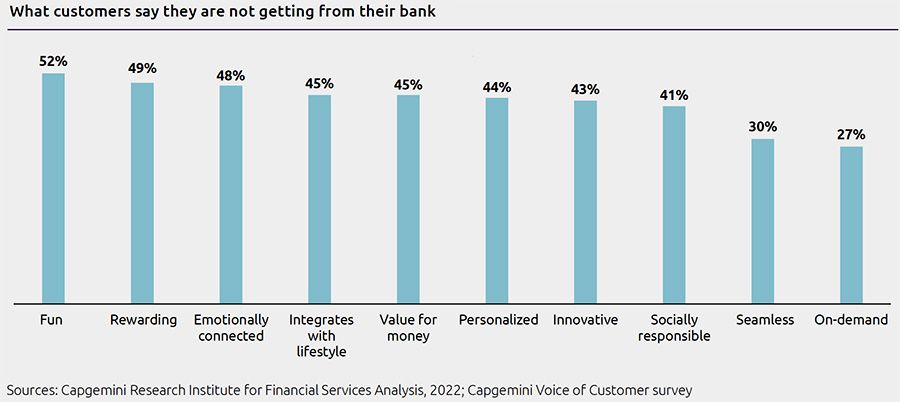

On the other hand, nearly half of those surveyed indicate that their current banking relationship is neither rewarding (49%) nor has an emotional connection (48%). Just over half (52%) of consumers do not like banking. To keep pace with their competitors, the researchers recommend that retail banks should rethink their business models, focusing on encouraging greater customer engagement.

Improved data governance models can be important in this regard, as it can help banks gather customer insights that can then be used to improve commercial competitiveness. Combining such models with AI and Machine Learning (ML) creates new opportunities to identify, retain and excite customers with real-time content.

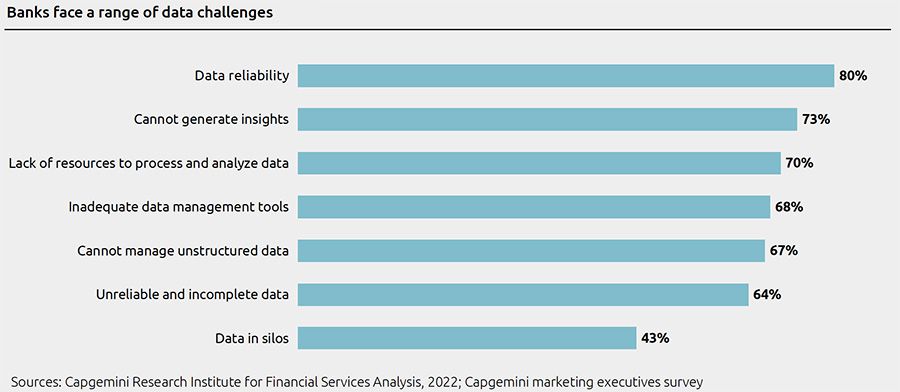

However, the researchers argue that many of these benefits are lost to traditional banks because they lack the capacity to handle all customer data. As many as 95% of top executives claim (in the qualitative survey portion) that outdated legacy systems and core banking platforms make data optimization and customer-focused growth strategies difficult, while 70% say they lack the resources to process and analyze data.

"The formula for growth sounds simple," states Alexander Eerdmans (Head of Financial Services at Capgemini Invent). "Customers want to be offered personalized experiences no matter where they are on their own digital journey. However, the challenge remains in execution."

Eerdmans explains that retail banks need to rethink their broader data models and focus on providing personalized journeys that customers expect based on all omnichannel interactions. "Real-time customer engagement requires a lot of data, systems and - not to mention - the human talent working on this. Traditional banks risk losing customer value to their more agile fintech and big tech counterparts."

To keep pace with more agile fintechs despite capacity shortages, established banks are combining traditional offerings with nonfinancial lifestyle products. Others offer Banking as a Service or embedded banking solutions through the ecosystems of non-financial third-party providers. Such platform models, according to the researchers, can do well in collecting data for personalization, making them well positioned to mine data ecosystems and derive real-time insights.

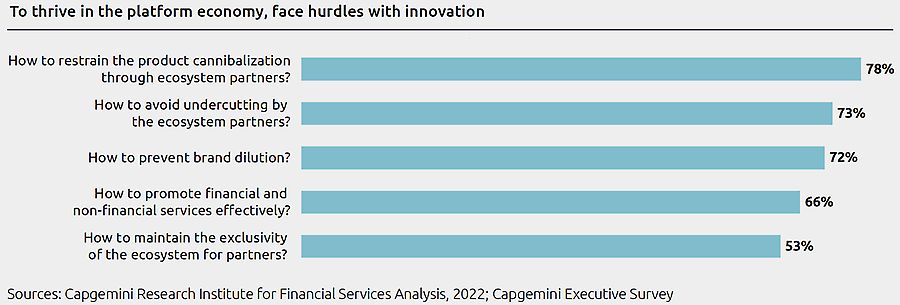

While such platform models are not new to banks, the survey shows that many players are still struggling with implementation. For example, 78% of senior executives claim to be concerned about cannibalizing products through ecosystem partners and 72% are concerned about brand dilution. The researchers argue, however, that the report shows that the challenges must be met.

"To thrive in this fiercely competitive environment, where digital native fintechs continue to capture an increasing share of the market value, we see retail banks finally embracing innovative technologies and platform models to optimize this data-driven growth," said Efma CEO John Berry.

"While this has evolved within the digital channels of many of these established banks, customers still expect bank branches to be experience centers, filled with self-service options and financial advice. By strengthening their ability to collect and analyze data, providers can identify what customers want: consistent omnichannel banking experiences."